Education Loan Process in India | Complete Guide

Education plays a pivotal role in shaping an individual’s future, and in a country like India, where quality education is highly valued, pursuing higher studies often requires financial support. This is where education loans come to help, providing students with the means to fulfil their academic aspirations. In this article, we will explain every important and small point of the education loan process in India.

The education loan process in India is designed to assist students in financing their academic endeavours while ensuring a smooth and hassle-free experience. Before getting into the details, it’s important to understand the significance of choosing the right bank. Numerous banks, financial institutions, Private Banks, and Cooperative banks offer education loans, each with its own set of terms and conditions. Conducting thorough research and comparing various options will help students find the most suitable loan for their specific needs.

Table of Contents

Education Loan Process in India: Understanding the Key Eligibility Requirements

1. Educational Institution Recognition: The college or university you plan to attend must be recognized by a competent authority or regulatory body.

2. Academic Performance: Lenders often consider academic merit as an important criterion. Students with a strong academic record are more likely to secure loans with favourable terms.

3. Admission Confirmation: Students should have secured admission on a merit basis through an entrance test or any other process of selection. You will need to provide proof of admission to the desired educational institution, such as an admission letter or fee receipt.

4. Co-applicant/Guarantor: Most education loans require a co-applicant or guarantor, who is usually a parent or guardian. Their financial stability and creditworthiness play a crucial role in the loan approval process.

5. Minimum marks for education loan is as under:

| General | 60% |

| OBC | 55% |

| SC/ST | 50% |

6. Age is not an important criterion for an education loan, even if the age of the student is below 18 years then his/her parents can join them as co-applicant in this loan and parents can execute the documents on behalf of the student. After attending the majority means 18 years students should sign a fresh set of documents for a loan.

7. Education Loans can also be sanctioned for pursuing courses under the management quota. However, only government-approved fees will be sanctioned.

Role of Co-Applicants : Who Can Join Co-Applicant for Education Loan

In the education loan process in India, the presence of a co-applicant can play a crucial role in obtaining financial assistance for higher studies. A co-applicant is an individual who shares the responsibility of the loan with the primary borrower, ensuring repayment and increasing the chances of loan approval. When considering who can be a co-applicant for an education loan, it is essential to understand the eligibility criteria set by lenders.

Typically, immediate family members such as parents or legal guardians are preferred choices as co-applicants. Their involvement brings a sense of financial stability and support, which enhances the lender’s confidence in loan repayment. Moreover, lenders may also consider spouses or siblings as eligible co-applicants in some cases.

The co-applicant’s role extends beyond just providing their name on the loan application. They are expected to contribute to the loan repayment process, and their income, credit history, and financial standing are evaluated by the lender to assess their overall repayment capacity. It is crucial to choose a co-applicant who has a stable income, a good credit score, and a strong financial background to increase the chances of loan approval.

Before finalizing a co-applicant, it is advisable to check the specific requirements of the chosen lender. Some financial institutions may have additional criteria or restrictions, so it is essential to review their guidelines to ensure compliance. By carefully selecting a qualified co-applicant in the education loan process, students can improve their chances of securing the necessary funding for their academic pursuits. A reliable co-applicant’s involvement not only strengthens the loan application but also provides reassurance to lenders, paving the way for a smoother and more successful education loan journey.

Eligible Courses

Education loans provide valuable financial assistance to students pursuing various courses. In the education loan process, eligibility criteria for courses play a significant role. Eligible courses for education loans in India encompass a wide range of disciplines, including engineering, medicine, management, law, arts, and technical fields like computer science, all the courses for which 10+2 is eligible for admission are eligible for an education loan, vocational courses of skill development courses, Courses approved by Central Government/State Government/AICTE/ICMR, Courses affiliated with recognized Universities. It’s important to note that each lender may have specific requirements regarding course recognition and institution affiliation. By understanding the eligible courses for education loans, students can navigate the education loan process more effectively, securing the necessary funds to pursue their academic aspirations.

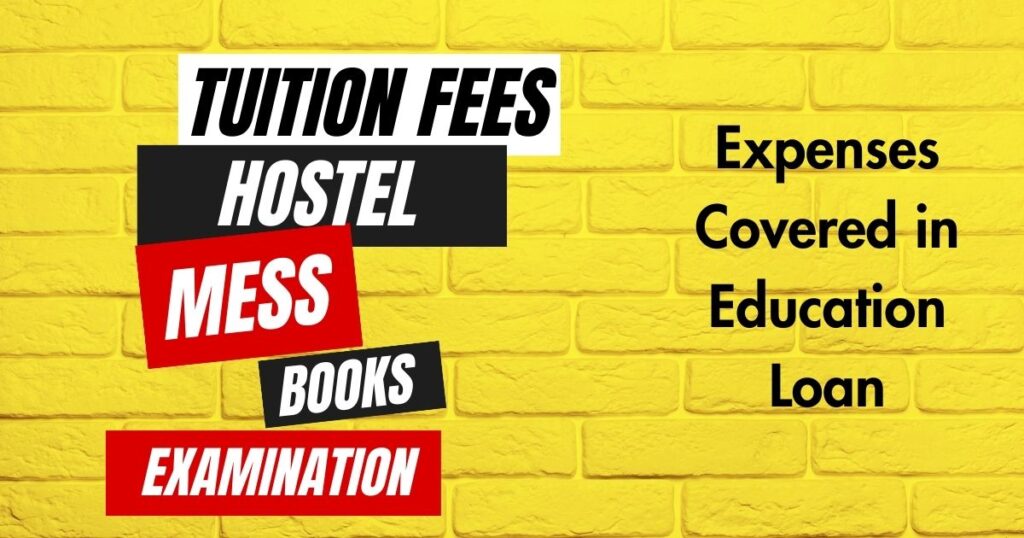

Expenses Covered in Education Loans in India

Education loans in India offer coverage for a wide range of expenses, providing essential financial support to students. Understanding the expenses covered in the education loan process is crucial for planning and managing funds effectively.

- Tuition fees

- Hostel charges

- Mess charges

- Examination

- Library Fee

- Laboratory fee

- Books and Stationary

- Laptop if required for the course

- Caution Deposit

- Study Equipment

- Expenses for a Study Tour

All these expenses should be mentioned in the fee structure of the institute.

Additional Expenses:

- Insurance premium of student

- If the Hostel facility is not available then students can opt to take accommodation separately but the cost of this accommodation should be justified.

Most banks do not consider development fees for education loan expenses unless the institute specifically explained that these development fees are used for educational purposes only.

Loan Amount

You can get 100% loan amount for education loan up to 4 lahks and above 4 lakhs you can get 95% loan, 5% margin money should be contributed by yourself. No upper or Lower limit is specified for education loan but all expenses should be justified.

Education Loan Interest Rate

- Simple interest during the course/moratorium period.

- Compounding rate of interest after the course/moratorium period.

- Servicing of interest during the course/moratorium period is optional for the borrowers.

- The accrued interest during the course/moratorium period will be added to the principal amount while fixing EMI for repayment.

| Bank | Loan Limit | Effective Interest Rate | Rate Type |

| SBI | No limit | 11.15% | Floating |

| Union Bank | Upto Rs. 7.50 lakhs | 11.30% | Floating |

| Union Bank | Above Rs. 7.50 lakhs | 10.90% | Floating |

| Canara Bank | Upto Rs. 7.50 lakhs | 11.25% | Floating |

| Canra Bank | Above Rs. 7.50 lakhs | 10.85% | Floating |

| Bank of Maharashtra | Upto Rs. 7.50 lakhs | 11.30% | Floating |

| Bank of Maharashtra | Above Rs. 7.50 lakhs | 10.95% | Floating |

Most Important: Some people assume that interest will charge after the moratorium period but it’s totally wrong, For the accounting purpose, interest booking will be done every month end, and this interest will not demand by the bank during the moratorium period, this accrued interest will added to the principal to calculate EMI after the end of the Moratorium period. Applicants can pay this interest but it’s completely optional and not mandatory at all.

Fee / Charges for Education Loans in India

| Processing Charges | Most Banks are not charging processing charges on Education Loan |

| Overdue Charges | Overdue Charges or penal interest @2% will be charged on the overdue amounts and overdue period. |

| Prepayment Penalty | No prepayment penalty |

| Take-over penalty | No prepayment penalty |

| Legal & Valuation Charges | Wherever property is offered as security for Education Loan in India, the borrower has to bear the Professional fee advocate for legal search and the Professional fee of the valuer for the valuation of the property proposed to be mortgaged. |

| Stamp duty | As per the state stamp act |

| Vidya Laxmi Processing Charges | Rs 100/- + GST as Portal Charges |

Guarantee Scheme for Education Loan in India

To promote Education Loan to deserving students who are not able to give security or guarantee to banks. The Government of India gives credit guarantee cover for Education Loan up to 7.50 lakhs through CGFSEL (This is explained in detail further in the article ). Banks never ask for security for education loan up to 7.50 lakhs.

Security for Education Loans above 7.50 lakhs

For loan above 7.50 lakhs, banks ask enforceable security for your education loan. Types of securities accepted by banks for Education Loan is as follows:

- Collateral security of minimum value equivalent to the loan amount.

- Property in the name of a family member.

- 3rd party security is also acceptable, provided the property owner joins in as co-applicant or guarantor.

- Identifiable (Fenced or Compounded Open plot) Open Plot/Land as Collateral Security accepted but it should be Non-Agricultural.

- Agriculture land is not accepted as security for education loan.

- Property having good connectivity of roads.

- Govt. securities/ Public Sector Bonds/NSC, KVP, life policy, gold, and bank deposit in the name of student/parent/guardian / other immediate family members (mother/ brother/ sister/ spouse) also acceptable to the bank.

Disbursement of Education Loan

- Education loan is sanctioned for full course duration as per the fee structure provided by the education institute. Disbursement of education loan will be on yearly basis before the commencement of the course every year.

- For example, if Your course fee for one year is Rs. 1 lakh then the total fee for 4 years is 4 lakhs, so banks disburse Rs. 1 lakhs every year before the commencement of education year after your written request.

- Further disbursement is done by the bank only after providing a passing certificate for the previous year. Suppose sometimes a student fails a previous exam and reappears to the exam and passes only then the bank will disburse for the next year.

- Even if you take a gap from education due to some unavoidable reason then also the bank will disburse the loan for the remaining course after proper justification by students. extension of time for completion, of course, can be permitted for a maximum period of 2 years.

- Wherever margin is applicable you need not pay full margin at a single time, it will be bifurcated on yearly basis as per your disbursement schedule.

- Most of the time students have to pay fees at the time of admission to confirm the admission seats so you can claim Reimbursement of those fees in your education loan subject to providing proper receipt of advance payment. (Please note: it is only applicable for the first year only, so do not pay fees that are already sanctioned by the bank for the second year onwards)

Repayment Period for Education Loan to Study in India

Maximum repayment tenure will be 15 years across all the banks fixed by RBI. For Example: For 4 Years Engineering Course

| Course Period | 48 Months |

| Job Searching Period | 12 Months |

| EMI calculated for | 120 Months |

| Maximum Loan Tenure | 180 Months |

Loan to be repaid by way of Equated Monthly installments (EMIs). The accrued interest during the moratorium period (if not serviced) is to be added to the principal amount while calculating Equated Monthly Installments (EMI) for repayment. In case the student discontinues the course midway, he/she should be asked to repay the loan immediately. That’s the main reason why banks finance education loan to Meritorious students only

Maximum Moratorium Period for Education Loan

If your course is of 4-year duration the Moratorium period is 4 years (Course Period) + 1 Year time given to search Job or Employment then your EMI is calculated for the remaining period of 10 years

Is insurance mandatory for Education loans?

As most of the loan are unsecured or covered under CGFSEL so Loan insurance policy for the student is mandatory in all banks and it should be assigned to the bank. Insurance policy should cover the life of the student for the tenure and quantum of the loan. A Premium amount can be included in the loan amount if requested by the applicant.

List of Documents Required for Education Loan

- Application form duly filled by the customer.

- KYC documents for each applicant / co-applicant / guarantor (if any):

- Identity proof (Pan card/Voters ID/Passport/Aadhaar Card etc)

- Residence proof (Driving license/ Passport/Electricity B1ll etc)

- Office/Business address proof of the Co-Applicant

- Latest passport size photograph

- ITR or Form 16 or Income proof of Borrower/Co-borrower/Guarantor, if any

- Last 12 months’ bank statement of Borrower/Co-borrower/Guarantor

- Caste certificate wherever required for statistical purposes only.

- You should bring all original documents for verification purposes only.

Academic documents required for Education Loan:

- Admission letter

- Mark sheets and certificates of all previous exams passed

- Fees Structure provided by the institution

- Bonafide

Education Loan for Two children or students from the same family

This loan is financed on individual capacity, you can apply for an education loan for more than one child also. In every education, loan parents are the Co-Applicant.

Can I get a Second Education Loan for Higher studies?

You can get additional education loan for higher studies also like a Master’s or Ph.D. etc, but you have to apply separately for this second loan. The moratorium period for an existing loan can also be increased till the master’s study completes.

A loan up to 4 lakhs is sanctioned without a third-party guarantee and if your total loan amount is more than 4 lakhs then you have to give a suitable third-party guarantee.

Rejection of Education Loan

Those days are gone when banks are hesitating to give education loan, now Government of India provides Credit Guarantees for education loan so banks are not simply rejecting education loan, and whenever there is any justifiable reason to reject the loan then that loan application will review by next higher authority and then it will get rejected.

Service area Norms for Education loan

Sometimes some banks will refuse to accept loan applications giving the reason that your residential address is not under their service area for sanctioning the education loan. But keep in mind This scheme is applicable all over India. The concept of the service area is not applicable to sanctioning Education Loan in India.

Still apply for an education loan in the branch nearest to the residence or where you or your parents are maintaining savings bank accounts. Parents and students should understand if a bank is available as mentioned above then why you are applying for an education other than that bank and if you are doing so then there should be acceptable justification.

Credit Guarantee Fund Scheme for Educational Loan (CGFSEL):

The government of India notified Credit Guarantee Fund Scheme for Educational Loan (CGFSEL) vide Gazette Notification No. 18-1/2013-U.5 (Vol. Ill) dated September 16, 2015.

The Credit Guarantee Fund Scheme for Education Loans (CGFSEL) is an integral part of the education loan process in India. It is a government-backed initiative aimed at providing financial support and security to lenders and borrowers in the education loan sector. CGFSEL acts as a guarantee mechanism, whereby eligible education loans are covered up to a certain limit, reducing the risk for banks and other financial institutions. This initiative allows lenders to provide education loans to deserving students who may not have sufficient collateral or a co-applicant. The CGFSEL helps streamline the education loan process, making it more accessible and inclusive for aspiring students across the country.

National Credit Guarantee Trustee Company Ltd. (NCGTC) has been set up by the Government of India to act as a common trustee company to manage and operate various credit guarantee trust funds.

Central Government Interest Subsidy Scheme for Education Loan in India:

GOI has launched a scheme of Interest Subsidy on educational loan for economically weaker sections of society. The students who satisfy all the following parameters would only be eligible for the interest subsidy:

- The scheme is applicable to inland studies only.

- The professional/technical courses are approved by NAAC-accredited Institutions.

- Under the CSIS scheme, only those education loan are eligible and are sanctioned without any collateral security or third-party guarantee.

- The subsidy is available up to a maximum amount of Rs.7.50 lakh irrespective of the sanctioned amount

- Annual gross family income from all sources should not exceed Rs. 4.50 Lakh.

- The student should furnish the income certificate issued by the competent authority and submit the same to the branch from where the loan is availed.

- Aadhaar no. is mandatory for claiming the subsidy.

- The interest subsidy is towards the interest charged in the loan account during the course and moratorium period only.

Sanction Process step by step explained

Step 1. Students have to apply for education loans through the Vidya Laxmi portal, it’s a government website, and all the applications are invariably routed through this portal.

Step 2. You have to fill basic details and preferences of two banks while filling out the form on the Vidya Laxmi portal and take the printout of the form. Remember to select a branch that is nearer to your address and where you already have a savings bank account.

Step 3. Visit the branch and submit all the required documents mentioned above already along with the printout form of the Vidya Laxmi portal.

Step 4. Your Bank will verify the details you provided and process the loan, the bank will verify the details of the fee structure and admission letter with your institute.

Step 5. An application that is received completely in all respects, will get sanctions within 7 working days in most banks.

Step 6. Bank will inform you as soon as your education loan will be sanctioned and hand over the Sanction letter of the education loan to you.

Step 7. Read the Sanction Letter carefully and understand the terms of the sanction.

Step 8. The bank will call you into the branch for signing the legal document for the education loan.

Step 9. After executing loan documents you can give a request for disbursement of the loan for payment of fees for the First Year.

Step 10. You have to submit bills and payment receipts to the bank for confirmation of the end use of funds

Vidya Laxmi Portal

Vidya Laxmi Portal is a web-based portal, launched by the Central Government on 15th August 2015 for the benefit of students seeking Education loan. The portal is providing a one-stop shop for students to access information & make an application for education loan provided by banks. In order to popularize the scheme, All the Education loan applications will be routed through Vidya Laxmi Portal.

Special Education Loan for Premier Institutes (Online and Collateral free Upto Rs. 40.00 Lakhs)

Union Digital Education Loan – Special Education Loan Scheme For Premier Institutes – Apply Now

Baroda Education Loan to Students of Premier Institutions – Apply Now

SBI Scholar Loans – Apply Now

Bank of India Star Vidya Loan – Apply Now

Click here to Apply for Education Loan through Vidya Laxmi Portal

Frequently Asked Question

Q1: When does the Education Loan EMI start?

Answer: Education Loan EMI starts after one year from completion of the Course.

Q2: Is interest applicable during the moratorium?

Answer: Yes, interest is applicable and debited to your loan account but will be demanded only after the moratorium period.

Q3: How is Education Loan Interest Calculated?

Answer: Simple interest is charged for the moratorium period and after completion of the moratorium period accrued interest is added to the principal and reset EMI and from now onwards bank will charge compounding interest.

Q4: Can I get a 100% Education Loan?

Answer: The loan up to Rs. 4 lakhs margin is Nil so you can get a 100% education loan up to Rs. 4 lakhs.

Q5: Do the documents for an education loan vary from one bank to another?

Answer: No, almost all banks’ Education loan documents are similar.

Q6: Is a co-applicant necessary for an education loan?

Answer: Yes, parents mandatorily join as co-applicant but if parents are not alive then any close relative joins as a co-applicant.

Q7: What is the responsibility of a co-applicant in an education loan?

Answer: Co-Applicant is equally responsible for repayment in any loan including education loan.

Q8: Is co-borrower compulsory for education loan?

Answer: Yes, parents mandatorily join as co-borrower but if parents are not alive then any close relative joins as a co-borrower.

Q9: Is life insurance mandatory for education loan?

Answer: Yes, Life Insurance for students is mandatory in education loan, and premium funding is also available in education loan.

Q10: How many education loan can be sanctioned to a student at a time?

Answer: Only one education loan at a time but you can get an education loan for acquiring higher educational qualifications.

Q11: Can I get another education loan if I already have one in India?

Answer: Yes, you can get another loan for acquiring higher educational qualifications.

Q12: Can I take two education loan simultaneously?

Answer: Yes, you can have two education loan but for acquiring the higher educational qualification and after completion of the first course only.

Q13: I have housing property that is already mortgaged to the bank, can I give this property as collateral for the Education Loan?

Answer: You have to do the latest valuation of the property and if the latest value is sufficient to cover the education loan then you can offer this as continuing security to the education loan. For example Latest Value of Housing property (A) Rs. 40,00,000/-, The margin for Housing Loan (B) Rs. 4,00,000/-, the Outstanding Housing Loan (C) Rs. 10,00,000/-, the Balance Security Value of Housing Property available for Education Loan (A-B-C) Rs. 36,00,000/-